**Note: This blog post will make several references to Detroit’s master plan neighborhoods. If you would like to view a reference map of these neighborhoods to help orient yourself, please click here.

Overview

This edition of City of Change examines the density of mortgage deeds (the number of mortgage deeds per square mile), since mortgage activity is one of the strongest indicators of a neighborhood’s investment potential. Regardless of the purpose of the mortgage deed, the presence of mortgage activity can indicate a commitment by residents to remain in a neighborhood and can identify interest and confidence from other market actors as well.

For this analysis, mortgage activity is defined as any mortgage deed filed to a property, regardless of its purpose. These deeds may include new mortgages (indicating investment by new residents) as well as refinanced mortgages or second mortgages (indicating investment by current residents who plan to remain in their home). As with previous installments of City of Change, the data have been summarized for 840 Census block groups in the city of Detroit. The mortgage deed data are based on D3’s analysis of transactional data purchased from the Wayne County Register of Deeds and encompass two time periods: 2008-09 and 2012-13. To remain consistent with other installments of City of Change, this analysis excludes block groups with fewer than 10 residential structures surveyed in the 2009 Detroit Residential Parcel Survey.

It is important to note that recorded mortgage deeds are not the sole measure of neighborhood residential sales activity. Many of the sales transactions in Detroit are cash sales or land contracts, with no mortgage involved. According to American Community Survey data, only about 55 percent of owner-occupied housing units in Detroit have a mortgage. Nevertheless, mortgage lending continues to be a primary indicator of market strength and represents a reliable proxy for overall market interest in a neighborhood.

Mortgage Activity in 2008-09

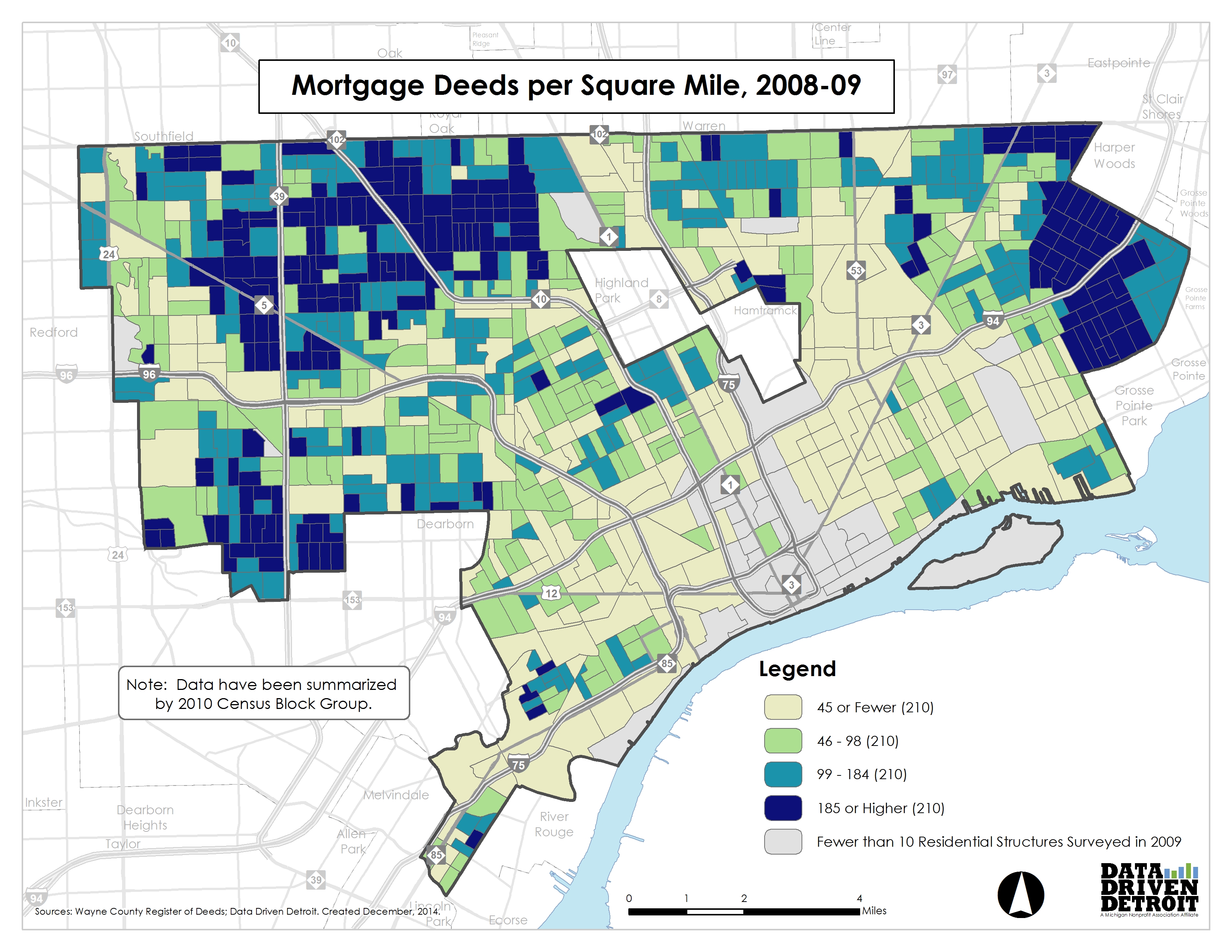

In 2008-09, the median mortgage density was roughly 100 deeds per square mile; that is, in 2008-09 half of all Detroit block groups had a mortgage density greater than 100. For individual areas, the density ranged from zero (no mortgages in the two-year period) to more than 550 mortgages per square mile. Figure 1 shows the mortgage density for each block group, divided into four equal ranges.

Figure 1:

This map shows mortgage deeds per square mile in 2008-09, divided into four equal ranges. The areas with the greatest amount of activity are the Far East, Northwest, and Far West portions of Detroit.

Mortgage activity in this period was generally concentrated in block groups in northwest Detroit, the Cody Rouge area, and the far east side, in the Finney and Denby master planning neighborhoods. The density of mortgage activity for most of the East Side between Woodward and Detroit City Airport falls in the lowest range. The same is true on the West Side, around and south of the Tireman master planning neighborhood.

Mortgage Activity in 2012-13

Across the city of Detroit, mortgage densities were also substantially lower in 2012-13 than in 2008-09, as shown in Table 1. The top range of block groups, which included 210 areas in 2008-09, contained only 62 block groups in 2012-13, a decrease of more than 70 percent. The bottom range, meanwhile, contained nearly 100 percent more block groups than it had in 2008-09.

Table 1: Change in Mortgage Deeds per Square Mile, 2008-09 to 2012-13

Figure 2 shows the geographic magnitude of these differences. Though certain areas of the Rosedale, Bagley, Palmer Park, and Finney master planning neighborhoods have remained in the top category, many others, including virtually all of Denby and Cody Rouge, are no longer in the top range.

Figure 2:

This map shows mortgage deeds per square mile in 2012-13, using the same ranges as 2008-09. The density of mortgage activity has contracted significantly in many areas across the city. Only a few areas – in particular, Indian Village and portions of Greater Downtown – clearly have greater mortgage density than in 2008-09.

Changes in Mortgages per Square Mile from 2008-09 to 2012-13

From 2008-09 to 2012-13, mortgage density declined in 685 block groups and remained the same in just 36. Only 119 block groups (14.2 percent) recorded an increase in mortgage deeds per square mile. As seen in Figure 3, these block groups are scattered across the city and include historic districts (Indian Village, Palmer Park, and Corktown) and middle-class neighborhoods (East Riverside and Rosedale). In the Corktown, Jeffries, and Lower Woodward master planning neighborhoods, the increase may be related to new residential construction activity. As seen in Figure 3, the block groups where there have been increases between the two-year periods in mortgage deeds per square mile include areas that recorded low mortgage densities in 2008-09 and those that were already active markets.

Meanwhile, the Finney/Denby and Cody Rouge master planning neighborhoods include many block groups that had high mortgage densities in 2008-09 but fell below the median by 2012-13. Several of the block groups west of Van Dyke (M-53) recorded substantial increases in mortgages per square mile but nevertheless remained in the bottom range.

Figure 3:

This map shows the change in mortgage deeds per square mile from 2008-09 to 2012-13. Increases have been limited mainly to the Greater Downtown area, the Woodward and Jefferson corridors, and the Rosedale Park neighborhood in Northwest Detroit.

It is important to recognize that this analysis is based on the ratio of mortgage recordings to geographic area during the two-year periods. Between 2008-09 and 2012-13, the number of recorded mortgages fell from 12,285 to 7,535, a decline of almost 39 percent. In 2012-13, there were only 52 block groups where more than 25 mortgages were recorded and just 10 where the number of new mortgages was greater than 50.

The median mortgage density has also declined substantially between the two-year periods. In 2012-13, it was just 46 mortgages per square mile, a decline of more than 50 percent from roughly 100 per square mile in 2008-09. In addition, while four block groups reported no mortgage activity in 2008-09, this number had swelled to 48 by 2012-13.

Conclusions

In summary, although 2008-09 was the beginning of the national mortgage crisis, Detroit’s experience then was much better than it was in 2012-13, when many other areas of the country had recovered. The citywide average mortgage density in 2012-13 was about 72 per square mile, compared to a residential structure density of about 1,800 per square mile. Moderate levels of mortgage activity occur in only a handful of areas in Detroit, and areas with increasing interest in mortgage investment appear to be confined largely to the city’s core, its historic neighborhoods, and a few other block groups scattered throughout the city.

City of Change will return next week with a look at Data Driven Detroit’s Dynamics Index, which is designed to identify areas of highest potential investment within the city.